by Dr. Travis A. Olds

Since the onset of the pandemic, millions of new miners have begun working to uncover raw resources; however, these miners are not the typical rock movers at your local quarry. They are instead making cryptographic calculations that reward newly minted digital currency – cryptocurrency.

You have likely heard a great deal about cryptocurrency lately, but may not understand what it is and may be wondering how something that doesn’t exist physically could hold any value? Gold and silver, as minerals with unique physical properties, have market value beyond that of currency, but consider for a moment the $20 bill. This paper currency itself has little physical value; it costs just under 14 cents to produce it, but the value of the bill is based on the fact that millions of people use and rely on it daily. The situation is similar for cryptocurrency. High demand for use and ownership of cryptocurrency creates its value.

Some cryptocurrencies have experienced a meteoric rise, and recently, an equally dramatic fall in value. The details are complex from a technical perspective, but people find crypto attractive for several reasons: using and owning it is significantly more secure than traditional banking, there are no limits to how much can be moved, and you can move it at any time. All transactions, even those made internationally, can be completed in just seconds and with significantly lower fees than those charged by traditional banks. Additionally, new mining methods, called “proof of stake,” even allow people to invest with crypto and earn interest over time.

Of course, there are new risks and controversies surrounding cryptocurrency that are not encountered in everyday banking and investing. Because crypto is decentralized, there is no governmental or organizational control, and this has many people questioning how to regulate and protect its use. Only a few vendors accept payments in cryptocurrency because of this. With conventional banking, every purchase, withdrawal, or deposit you make through a bank or credit union with cash or credit is tracked by an electronic ledger to verify and secure your activities. The government helps to regulate and ensure the safety of these required systems.

Cryptocurrency, on the other hand, uses a shared and system-wide electronic ledger called the “blockchain.” All transactions made through the blockchain are tracked, verified, and securitized using rapid cryptographic calculations made via individual miners. This ongoing electronic verification process ensures the massive digital transaction ledger cannot be controlled or altered by individual users. Crypto miners contribute to the ongoing verification process by operating machines to run the necessary calculations. A fraction of a freshly minted electronic coin is awarded for the cryptography calculations one miner does to help secure a transaction, what is termed the “proof of work” consensus mechanism.

Performing proof of work calculation consumes electricity. Globally, the amount of electricity used by crypto miners has increased exponentially since its inception and this has drawn controversy regarding its impact on our environment. Some large mining farms use more electricity in one day than most small cities or countries do in several; however, the total electricity used by crypto miners still makes up just a small percentage of that used by the traditional electronic banking and investing systems. In fact, traditional banking and crypto systems are both environmentally unfriendly in places that get their electricity from carbon-based power generation, such as coal, heating oil, and natural gas. In early 2022 here in Pennsylvania, 66% of our power came from carbon-based sources, with 30% from nuclear, and the remaining 3% from hydroelectric and other renewable sources. While that cocktail of energy sources makes electricity cheaper here than in most other states, it also means that Pennsylvanians indirectly emit considerably more carbon to keep their lights on. Coal, oil, and natural gas are the cheapest but also the three least efficient fuels for electricity generation and have collectively done the most harm to the environment.

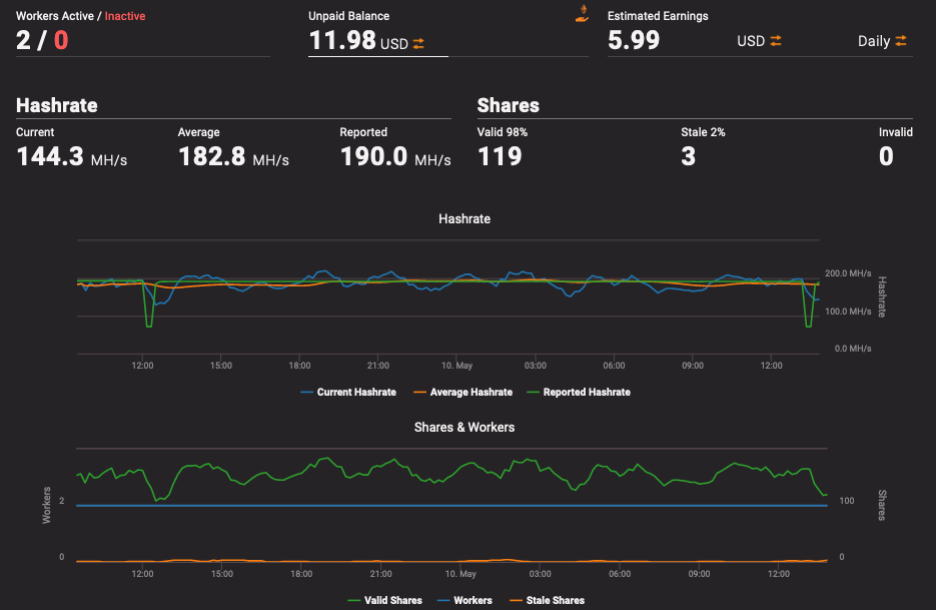

Specialized crypto mining hardware, including graphics cards and ASIC units, generates heat while performing rapid calculations, so it helps to mine in areas with cool weather. If the hardware can operate at a cooler temperature, it can perform more calculations, which is measured in hashes/second, and is used to quantify the rewards received. Many miners take advantage of the easy scalability of mining hardware, by building large farms that can contain thousands of graphics cards and make thousands of dollars per day, but that also consume enormous amounts of electricity.

Electrical inefficiency and negative environmental impact have encouraged some cryptocurrency coin developers to come up with more energy efficient algorithms for rewards, but implementation is a slow and complex process. Many miners focus on whichever cryptocurrency is most profitable on any given day, regardless of its efficiency. Many of the largest mining farms are built in areas where energy is cheapest, or where local governments provide property or other tax incentives. Typically, no consideration of environmental impact is made when establishing new farms. In contrast, small amateur and at-home miners with only a few graphics cards can mine cryptocurrency without much increase to their monthly electrical bill. It is possible to make a small profit if you live in an area with cheap electricity, or if you can offset the use with renewable energy, for example, by using solar panels. With two graphics cards, one can make up to $6 a day mining Ethereum, a currently extremely popular crypto coin.

The visible costs to start mining include buying the hardware, which can cost up to several thousand dollars, and paying for the electricity to power it. A mining “rig” with two graphics cards consumes 600 W, and costs $1.50 per day to mine $6 of Ethereum. Put that another way, the electricity needed to realize a $4.50 profit in one day is equivalent to leaving a 60W light bulb on continuously for 10 days. The invisible and usually overlooked cost of that profit is how roughly two-thirds of the electricity needed to profit was generated by burning fossil fuels and has indirectly but significantly contributed to climate change.

Cryptocurrency is fraught with inefficiency, complexity, and controversy. The framework is constantly evolving and improving, and although it is far from replacing the day to day use of physical currency, many argue that digital currency is here for the long run. The development of less power-intensive mining methods and more energy efficient hardware is helping to offset the carbon footprint of crypto mining. Crypto mining will become more environmentally friendly in the future, as nuclear power and other renewables like solar and wind energy become cheaper, replacing the dirty and archaic coal and natural gas-burning power stations.

Dr. Travis A. Olds is Assistant Curator of Minerals at Carnegie Museum of Natural History.

Related Content

Understanding Fossil Fuels Through Carnegie Museums’ Exhibits

Sea Snails from Christmas Island (Money Cowries and Castor Bean Shells)

Carnegie Museum of Natural History Blog Citation Information

Blog author: Olds, Travis A.Publication date: June 1, 2022